Yesterday we posted an article which suggested that the chef-owner of a restaurant will generally contribute both labour and capital and therefore should be aware that (s)he should be financially rewarded for both, being an appropriate salary (for the labour) and an adequate return on capital by way of profit (we estimated 20% per annum). The most common push-back to the post was that we had not taken into account the fact that at some point in the future, the owner might sell the restaurant, making a gain on sale, and this would potentially compensate for a shortfall in adequate returns in earlier years.

This follow on post considers whether gains on sale should in fact be factored into business plans as an acceptable alternative to earlier cash distributions to the owner. We strongly believe the answer is no, they shouldn't, and that if a gain on sale is achieved, it should be considered an unexpected bonus.

What's a business worth?

If you are are to factor into your restaurant business plan a sale at a later date, you need to have some idea how to value the business. It is our view that a sensible valuation can be derived by considering that the ratio of the value of the restaurant to the equity in the restaurant is in direct proportion to the return on that equity versus the cost of equity.

Mathematically, that is represented by the formula Sale Price/Equity = ROE/cost of equity

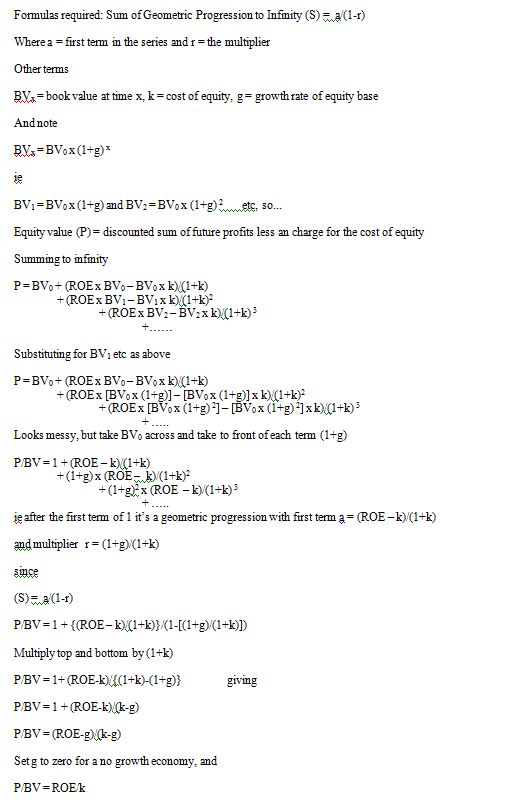

For those interested in where this comes from, we include our derivation of this formula here and note that it is a widely accepted valuation tool in the world of finance. Things are now quite easy. At the outset of a potential investment, we stated previously that the cost of equity was (most probably) at least 20%. Very simply then, if the business itself makes a 20% return on capital, then the value of the business (potential sale price) is equivalent to its equity value so there is no gain on sale.

Is this, an estimated 20% ROE, reasonable? For most restaurants, the profits they make are private, so it's hard to provide hard data about the industry in general, but we can still find examples where profits are disclosed. Smiths of Smithfield trades through a limited company (Smiths of Smithfield Ltd) and so files accounts with Companies House which are available to the public for the sum of £1. SOS would have to be considered a very successful restaurant in our view and in their most recently filed accounts (for the year to 31 May 2011), they made post tax profits of £183,812 on an equity base of £1,054,967 (at the start of their year). Approximately then, they achieved a 17.4% ROE. Unless there has been a meaningful uptick in trading performance subsequently, we might reasonably say that Smiths of Smithfield, if it were to be sold, might come to the market at a price of £1.0 - 1.2mn with no real capital gains for the owners.

Put another way, without some kind of financial engineering, you have to believe that a restaurant is going to be a huge success financially to anticipate a gain on sale.

But assuming you do get a gain...

If significant debt is utilised however, it might be possible to use leverage to achieve superior returns (compared to the cost of capital), and that in turn would give you a potential gain on sale, so is that the answer? A simple model below considers this particular example.

Here, the initial restaurant opening capital of £500,000 is now only 50% equity with a further 50% bank debt. Return on total capital is 20% giving £100,000 of profit. However, debt costs must now be deducted from that, which we charge at 10%, leading to a very respectable profitability of 30% Return on Equity (75,000/250,000 x 100%). Each year then, for the first five years, we assume a salary paid to the owner of £30,000 post tax, and a dividend from profits of £75,000. This is without doubt a very good business for the owner, with £105,000 extracted each year as cash paid to him/her.

At the end of year five, we assume an immediate sale. In line with our above formula, the business sells at 1.5x the equity value (30% ROE/20% cost of equity), and that means a capital gain of £125,000 (50% x £250,000) for the owner. However, at the planning stage, all of these cash flows are between one and five years in the future and need to be discounted back at the appropriate cost of risk.

When this is done, the net present value (NPV) of future cash flows is £419, 468, while the gain on sale five years down the line is worth in today's money £66,200, so just 15.8% of the overall value of the business. Note that without that gain, the business would have enjoyed a NPV of £353,268 for an initial investment of £250,000 so would still have been worthwhile and the gain on sale comes as a nice bonus but is not the deciding factor in whether this business should be undertaken.

This follow on post considers whether gains on sale should in fact be factored into business plans as an acceptable alternative to earlier cash distributions to the owner. We strongly believe the answer is no, they shouldn't, and that if a gain on sale is achieved, it should be considered an unexpected bonus.

What's a business worth?

If you are are to factor into your restaurant business plan a sale at a later date, you need to have some idea how to value the business. It is our view that a sensible valuation can be derived by considering that the ratio of the value of the restaurant to the equity in the restaurant is in direct proportion to the return on that equity versus the cost of equity.

Mathematically, that is represented by the formula Sale Price/Equity = ROE/cost of equity

For those interested in where this comes from, we include our derivation of this formula here and note that it is a widely accepted valuation tool in the world of finance. Things are now quite easy. At the outset of a potential investment, we stated previously that the cost of equity was (most probably) at least 20%. Very simply then, if the business itself makes a 20% return on capital, then the value of the business (potential sale price) is equivalent to its equity value so there is no gain on sale.

{kind=link}

Is this, an estimated 20% ROE, reasonable? For most restaurants, the profits they make are private, so it's hard to provide hard data about the industry in general, but we can still find examples where profits are disclosed. Smiths of Smithfield trades through a limited company (Smiths of Smithfield Ltd) and so files accounts with Companies House which are available to the public for the sum of £1. SOS would have to be considered a very successful restaurant in our view and in their most recently filed accounts (for the year to 31 May 2011), they made post tax profits of £183,812 on an equity base of £1,054,967 (at the start of their year). Approximately then, they achieved a 17.4% ROE. Unless there has been a meaningful uptick in trading performance subsequently, we might reasonably say that Smiths of Smithfield, if it were to be sold, might come to the market at a price of £1.0 - 1.2mn with no real capital gains for the owners.

Put another way, without some kind of financial engineering, you have to believe that a restaurant is going to be a huge success financially to anticipate a gain on sale.

But assuming you do get a gain...

If significant debt is utilised however, it might be possible to use leverage to achieve superior returns (compared to the cost of capital), and that in turn would give you a potential gain on sale, so is that the answer? A simple model below considers this particular example.

Here, the initial restaurant opening capital of £500,000 is now only 50% equity with a further 50% bank debt. Return on total capital is 20% giving £100,000 of profit. However, debt costs must now be deducted from that, which we charge at 10%, leading to a very respectable profitability of 30% Return on Equity (75,000/250,000 x 100%). Each year then, for the first five years, we assume a salary paid to the owner of £30,000 post tax, and a dividend from profits of £75,000. This is without doubt a very good business for the owner, with £105,000 extracted each year as cash paid to him/her.

At the end of year five, we assume an immediate sale. In line with our above formula, the business sells at 1.5x the equity value (30% ROE/20% cost of equity), and that means a capital gain of £125,000 (50% x £250,000) for the owner. However, at the planning stage, all of these cash flows are between one and five years in the future and need to be discounted back at the appropriate cost of risk.

When this is done, the net present value (NPV) of future cash flows is £419, 468, while the gain on sale five years down the line is worth in today's money £66,200, so just 15.8% of the overall value of the business. Note that without that gain, the business would have enjoyed a NPV of £353,268 for an initial investment of £250,000 so would still have been worthwhile and the gain on sale comes as a nice bonus but is not the deciding factor in whether this business should be undertaken.

In summary

The conclusion must surely be that actually, you simply can't get away from the benefit of modelling the cash flows with sensible assumptions in order to make a good decision, but beyond that, the capital gain should not in our mind be the decisive factor for three reasons:

1) the restaurant needs to be excessively profitable to make a gain in the first place, and deciding to start a profitable business is an easy decision so it will never hinge on the gain.

2) the gain on sale is the very last cash flow you receive from the business and therefore enjoys the largest discount factor reducing its relative contribution to the total (even if nominally it seems a large number), and

3) the uncertainty surrounding any forecast that is at least five years out means that it is your least reliable assumption within your whole business plan. Do you really want the decision to invest, or not, to be decided on your least reliable assumption?

This is clearly a complex area but we hope the above discussion clearly illustrates why the key factor in making an initial investment needs to be an ongoing profitable business, and not an indeterminate capital gain that might otherwise trick you into an incorrect financial decision.

Read the previous article: Is your restaurant making enough money?

The conclusion must surely be that actually, you simply can't get away from the benefit of modelling the cash flows with sensible assumptions in order to make a good decision, but beyond that, the capital gain should not in our mind be the decisive factor for three reasons:

1) the restaurant needs to be excessively profitable to make a gain in the first place, and deciding to start a profitable business is an easy decision so it will never hinge on the gain.

2) the gain on sale is the very last cash flow you receive from the business and therefore enjoys the largest discount factor reducing its relative contribution to the total (even if nominally it seems a large number), and

3) the uncertainty surrounding any forecast that is at least five years out means that it is your least reliable assumption within your whole business plan. Do you really want the decision to invest, or not, to be decided on your least reliable assumption?

This is clearly a complex area but we hope the above discussion clearly illustrates why the key factor in making an initial investment needs to be an ongoing profitable business, and not an indeterminate capital gain that might otherwise trick you into an incorrect financial decision.

Read the previous article: Is your restaurant making enough money?